We are not meeting Paris ambitions

We are not meeting Paris ambitions; there is a short window of opportunity to close the gap

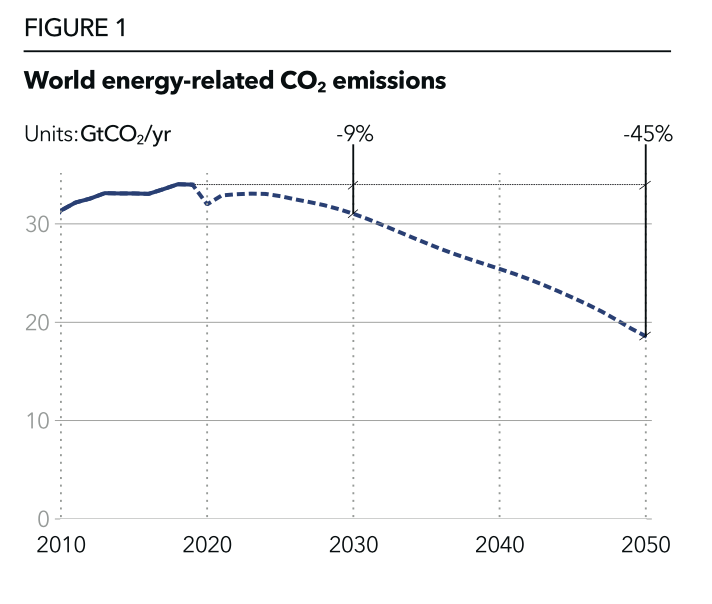

Global emissions likely peaked in 2019, followed by an unprecedented 6% drop in 2020 due to COVID-19. Emissions are now rising sharply again and will grow for the next three years before starting to decline.

While they are being added at great speed, renewables currently often supplement rather than fully replace thermal power generation. By 2030, global energy-related CO2 emissions are likely to be only 9% lower than 2019 emissions, and by 2050 only 45% lower. This is in sharp contrast to ambitions to halve GHG emissions by 2030 and to achieve the net zero emissions by 2050 required to limit global warming to 1.5 ̊C. Our forecast is that we are most likely headed towards global warming of 2.3 ̊C by 2100.

As CO2 emissions continue to accumulate, the window of opportunity to act narrows every year. Relying on large- scale net-negative emissions technologies and carbon removal in the latter half of the century is a dangerous, high-risk approach. With global warming, every fraction of a degree is important, and all options to reduce emissions need urgent realization.

Fossil fuels are gradually losing position, but retain a 50% share in 2050

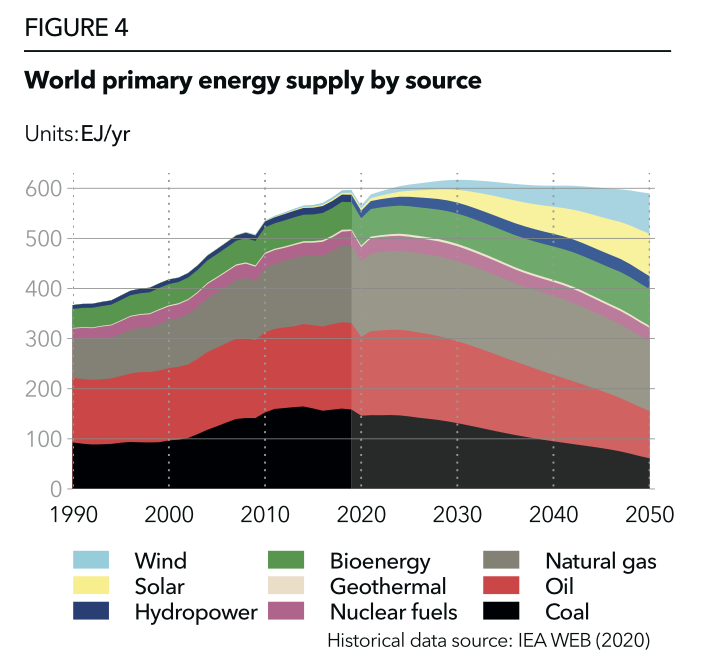

Fossil fuels have held an 80% share of the global energy mix for decades. DNV forecast that, by mid-century, fossil fuels will decrease, but still hold a 50% share of the energy mix, a testament to the inertia of fossil energy in an era of decarbonization.

Coal use will fall fastest, down 62% by 2050. Oil use stays relatively flat until 2025 when it starts a steady decline, to just above half of current levels by mid-century. Gas use will grow over the coming decade, then levels off for a 15-year period before starting to reduce in the 2040s. Gas will surpass oil as the largest energy source and will represent 24% of global energy supply in 2050.

Most hydrogen will be produced from dedicated renewables-based electrolysers by 2050

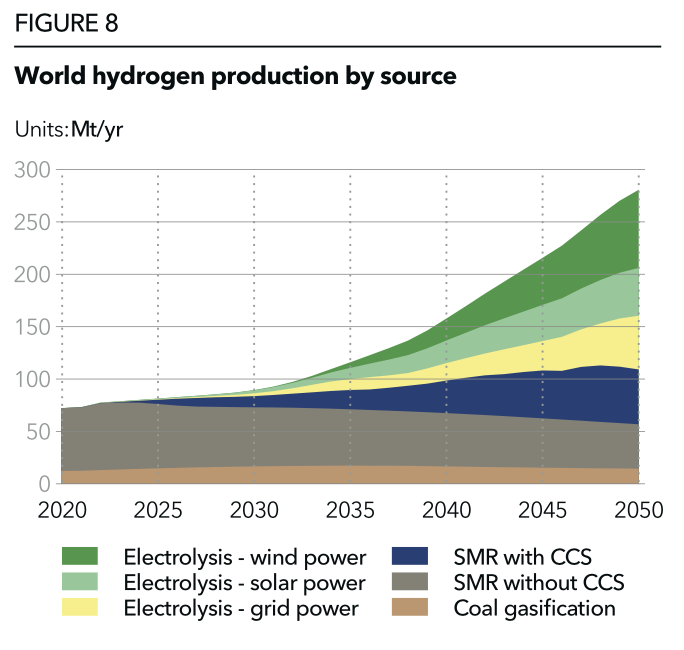

The current production of hydrogen as an energy carrier is negligible compared with the 75m tonnes of grey/ brown hydrogen produced annually for fertilizer and chemicals production.

Blue hydrogen, produced by steam methane reforming (SMR) from gas with CCS, will replace some of the grey and brown hydrogen in the coming decades. In total, blue hydrogen will also comprise 18% of hydrogen supply for energy purposes by 2050.

Green hydrogen from electrolysis will be the main long-term solution for decarbonizing hard-to-abate sectors, including hydrogen as a basis for other e-fuels.

Electrolysis powered by grid electricity is disadvantaged by the limited number of hours of low-priced electricity. Its CO2 footprint will, however, improve as more renewables enter the power mix. The future production of hydrogen for energy purposes will be dominated by electrolysis using dedicated off-grid renewables, such as solar and wind farms. By 2050, 18% of hydrogen will be grid-based and 43% will come from dedicated capacity comprising solar PV (16%), onshore wind (16%) and fixed offshore wind (9%).

Storage and flexibility

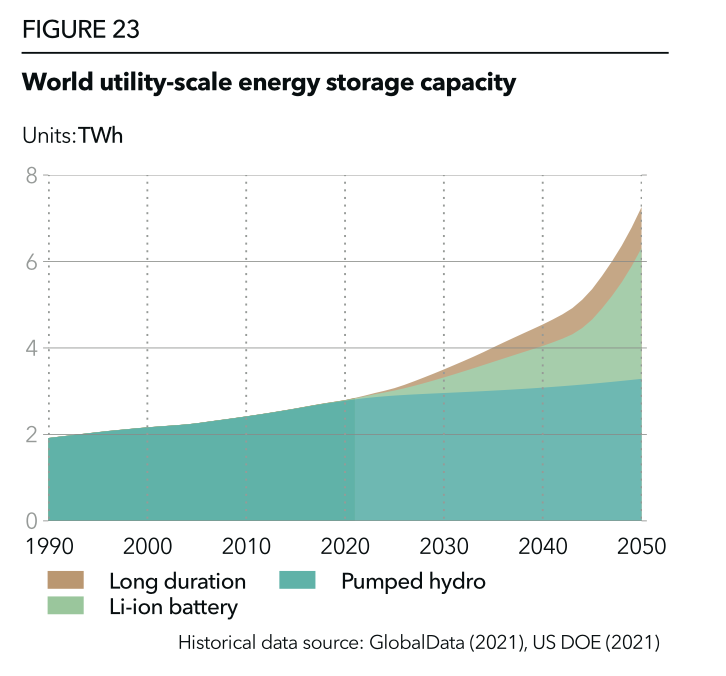

As we move towards a decarbonized electricity system, there is both opportunity and need for flexibility. With high shares of solar and wind, traditional sources of flexibility will need to be accompanied by a large amount of storage. Over the next 30 years, utility-scale storage capacity will grow 160% to reach 7.3 TWh.

With the value of flexibility increasing, many conventional generation technologies, like gas-fired power stations, will seek ways to accelerate their ramp rates and reduce their start times. There will be a growing emphasis on shifting electricity usage from peak periods to times of lower demand. Better prediction of renewable power generation – and also consumption – levels will evolve, and new technologies and market mechanisms will allow more consumers to provide flexibility in the form of demand response.

Converting cheap electricity from VRES to other energy carriers, such as hydrogen, will add more flexibility. Adoption of smart meters and smart grids, continued investment in the interconnectors between physical transmission systems, and in the links between generation and load centres, will also contribute towards better utilization of excess renewable supply.

Storage technologies will increasingly allow power generation to be decoupled timewise from power demand. Storage in today’s power system is mostly in the form of pumped hydro. Although it is a mature technology and limited by geography, pumped hydro is set to grow by 20% over the next three decades.

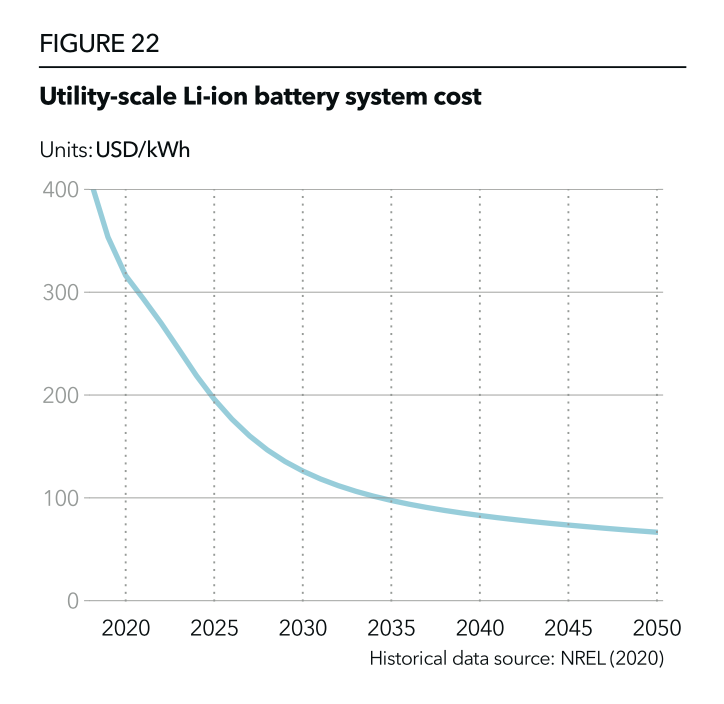

High penetration of wind and solar raises price variability and strengthens the business case for storage, as does the plunging cost of battery technology. DNV forecast widespread expansion of battery storage, dominated by Li-ion batteries with 2-4 hours capacity. From 2040 onwards, throughput of vehicle-to-grid systems in the world will be almost as large as that of dedicated Li-ion batteries and pumped hydro, reaching 240 TWh/yr globally by mid-century.

In larger markets for utility-scale battery storage (e.g., China, South Korea, Japan, US), demand for longer- duration storage (>5 hours) is already developing and will intensify. This trend will boost new technologies like vanadium redox flow batteries, zinc-based chemistries, or compressed air. Long-duration storage capacity is likely to be nearing 1 TWh by 2050.