Global Hydrogen Review 2021 – IEA Analysis

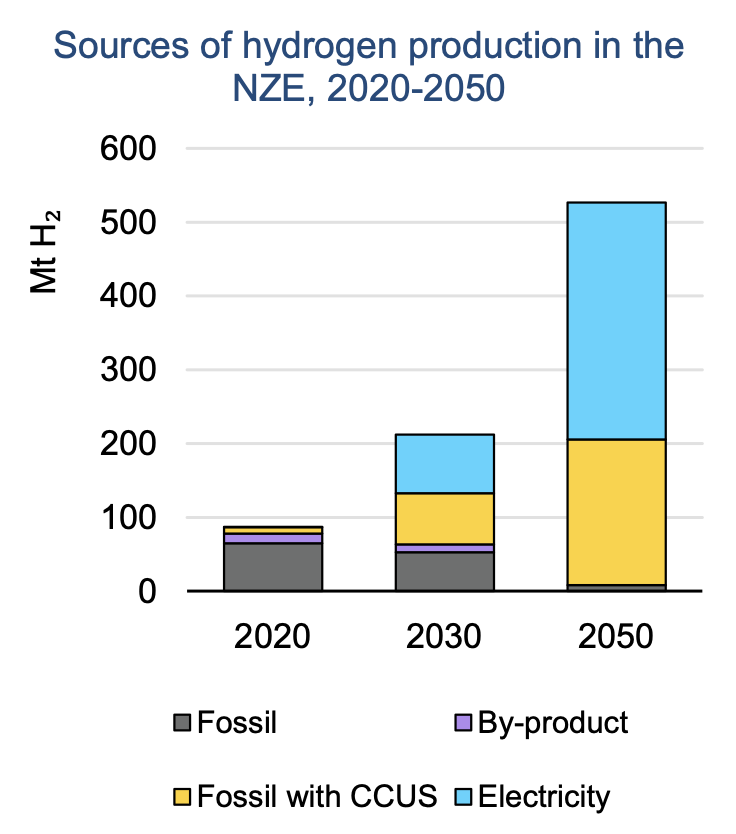

Hydrogen demand stood at 90 Mt in 2020, practically all for refining and industrial applications and produced almost exclusively from fossil fuels, resulting in close to 900 Mt of CO2 emissions. But there are encouraging signs of progress. Global capacity of electrolysers, which are needed to produce hydrogen from electricity, doubled over the last five years to reach just over 300 MW by mid-2021. Around 350 projects currently under development could bring global capacity up to 54 GW by 2030. Another 40 projects accounting for more than 35 GW of capacity are in early stages of development. If all those projects are realised, global hydrogen supply from electrolysers could reach more than 8 Mt by 2030. While significant, this is still well below the 80 Mt required by that year in the pathway to net zero CO2 emissions by 2050 set out in the IEA Roadmap for the Global Energy Sector.

Europe is leading electrolyser capacity deployment, with 40% of global installed capacity, and is set to remain the largest market in the near term on the back of the ambitious hydrogen strategies of the European Union and the United Kingdom. Australia’s plans suggest it could catch up with Europe in a few years; Latin America and the Middle East are expected to deploy large amounts of capacity as well, in particular for export. The People’s Republic of China (“China”) made a slow start, but its number of project announcements is growing fast, and the United States is stepping up ambitions with its recently announced Hydrogen Earthshot.

Sixteen projects for producing hydrogen from fossil fuels with carbon capture, utilisation and storage (CCUS) are operational today, producing 0.7 Mt of hydrogen annually. Another 50 projects are under development and, if realised, could increase the annual hydrogen production to more than 9 Mt by 2030. Canada and the United States lead in the production of hydrogen from fossil fuels with CCUS, with more than 80% of global capacity production, although the United Kingdom and the Netherlands are pushing to become leaders in the field and account for a major part of the projects under development.

Governments must take a lead in the energy transformation. In The Future of Hydrogen, the IEA identified a series of recommendations for near-term action. This report offers more detail about how policies can accelerate the adoption of hydrogen as a clean fuel:

- Develop strategies and roadmaps on the role of hydrogen in energy systems: National hydrogen strategies and roadmaps with concrete targets for deploying low-carbon production and, particularly, stimulating significant demand are critical to build stakeholder confidence about the potential market for low-carbon hydrogen. This is a vital first step to create momentum and trigger more investments to scale up and accelerate deployment.

- Create incentives for using low-carbon hydrogen to displace unabated fossil fuels: Demand creation is lagging behind what is needed to help put the world on track to reach net-zero emissions by 2030. It is critical to increase concrete measures on this front to tap into hydrogen’s full potential as a clean energy vector. Currently, low-carbon hydrogen is more costly to use than unabated fossil-based hydrogen in areas where hydrogen is already being employed – and it is more costly to use than fossil fuels in areas where hydrogen could eventually replace them. Some countries are already using carbon pricing to close this cost gap but this is not enough. Wider adoption combined with other policy instruments like auctions, mandates, quotas and hydrogen requirements in public procurement can help de-risk investments and improve the economic feasibility of low-carbon hydrogen.

- Mobilise investment in production, infrastructure and factories: A policy framework that stimulates demand can, in turn, prompt investment in low-carbon production plants, infrastructure and manufacturing capacity. However, without stronger policy action, this process will not happen at the necessary pace to meet climate goals. Providing tailor-made support to selected shovel-ready flagship projects can kick-start the scaling up of low-carbon hydrogen and the development of infrastructure to connect supply sources to demand centres and manufacturing capacities from which later projects can benefit. Adequate infrastructure planning is critical to avoid delays or the creation of assets that can become stranded in the near or medium term.

- Provide strong innovation support to ensure critical technologies reach commercialisation soon: Continuous innovation is essential to drive down costs and increase the competitiveness of hydrogen technologies. Unlocking the full potential demand for hydrogen will require strong demonstration efforts over the next decade. An increase of R&D budgets and support for demonstration projects is urgently needed to make sure key hydrogen technologies reach commercialisation as soon as possible.

- Establish appropriate certification, standardisation and regulation regimes: The adoption of hydrogen will spawn new value chains. This will require modifying current regulatory frameworks and defining new standards and certification schemes to remove barriers preventing widespread adoption. International agreement on methodology to calculate the carbon footprint of hydrogen production is particularly important to ensure that hydrogen production is truly low-carbon. It will also play a fundamental role in developing a global hydrogen market.